|

|

|

|

|

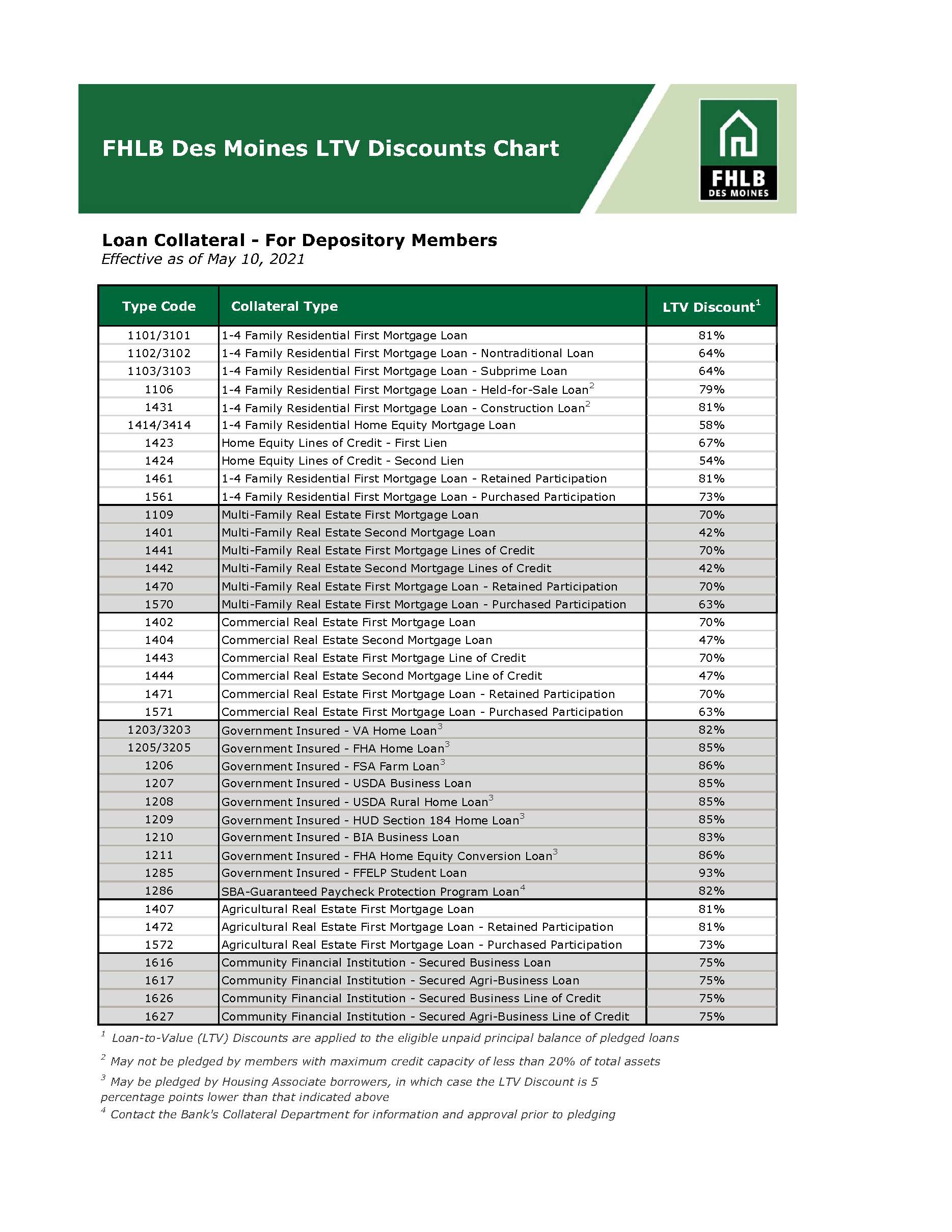

Updated Collateral Loan-to-Values Effective May 10

|

|

|

|

|

|

|

Employee Feature: Barbara Loper, Manager, Collateral Review Depositories

|

|

FHLB Des Moines (the Bank) periodically reviews our collateral Loan-to-Value (LTV) Discounts to ensure they are consistent with the current market environment. On May 10, 2021, FHLB Des Moines implemented revised LTVs for most collateral categories with many loan collateral categories increasing their LTV. These changes may affect your borrowing capacity with FHLB Des Moines.

|

|

|

|

|

|

|

|

|

|

Commercial Real Estate and Multi-Family Eligibility Changes

|

|

|

As a result of current conditions in the commercial markets, the Bank is adjusting select loan eligibility criteria commencing on June 30, 2021 as follows:

Maximum Property Loan to Values: The maximum property LTVs (loan’s UPB or credit line divided by the property’s value) are reduced by 10 percentage points for all commercial real estate and multi-family loan collateral types (e.g., the current maximum property LTV on 1109 Multi-Family First Mortgage and 1402 Commercial Real Estate First Mortgage loans is 85%; the revised limit is 75%).

Debt Service Coverage Ratio (DSCR): A minimum Property DSCR of 1.0x is required for loans/lines pledged by members executing the following Advances Pledge and Security Agreement (APSA) types:

- Non-Blanket APSA: All Loans

- Blanket APSA: Loans with Unpaid Principal Balance (or credit limits) ≥ $5,000,000.

Property DSCR:

- DSCR based on the fully amortizing payment supported by actual property net operating income (NOI) not > 18 months from reporting date. Supported by rent roll(s) not more than 13 months from reporting date.

- Proforma NOI based on executed leases and/or rent rolls that demonstrate a DSCR ≥ 1.0x acceptable for newly originated loans for up to 18 months following first operating calendar year-end. DSCR based on actual NOI required thereafter.

- For non-amortizing loans/lines, the DSCR is based on an amortizing payment equivalent with term no more than 30 years.

- Property NOI only (i.e. excludes non-property cash flows or guarantees); includes superior lien debt service.

Pre-Approval - Specific or Delivery APSA Members: New pledges of all commercial real estate and multi-family loans must be reviewed and approved in advance of providing lendable value.

The Bank will be revising eligibility checklists to reflect these changes as of the June 30, 2021 implementation date. Please contact the collateral department if you have questions on these changes.

|

|

|

|

|

|

|

|

New Collateral Type: Interest-Only Loans

|

|

|

|

|

|

|

Headline (H4)

|

|

We are excited to announce the Bank will soon be accepting interest-only loan collateral for Multi-Family (type code 1110) and Commercial Real Estate (type code 1410) loans (whole loans only, no participations).

Additional eligibility details will be posted on our website. Members interested in pledging this collateral type with a Specific or Delivery Advances, Pledge and Security Agreement (APSA) will need to notify FHLB Des Moines prior to pledging.

|

|

|

|

|

|

|

|

|

|

Expanded Clarity and Details for Loan Listing Files

|

|

|

|

Members who submit a monthly loan listing file using the expanded file format will see revised definitions and permissible values and a reduced number of required fields to help better clarify for members what information needs to be included in each field of the file.

No fields have been changed on the loan listing file itself, but it is important for members to enter all field information correctly to ensure the collateral remains eligible.

|

|

|

|

|

|

Collateral Reporting: Loans in Forbearance

|

|

|

For the past year, we have temporarily

adjusted eligibility guidelines on pledged collateral to align with our member financial institutions who are implementing loan forbearance or loan modifications agreements for their borrowers. Members are required to report details of pledged loans in forbearance on their Borrowing Base Certificate (BBC) and loan listing files accordingly.

We have published additional resources to help with this process, including:

- Events that would end forbearance and thus BBC reporting of forbearance

- Assistance for identifying and reporting loans at an individual loan level on the General File or the Expanded File formats

- Reporting loans with modifications that end forbearance

|

|

|

|

|

|

|

|

Guidance for LIBOR-Indexed Collateral Available This Month

|

|

|

With the phase out of LIBOR by June 30, 2023, FHLB Des Moines has taken several steps over the past few years to help members through this transition.

Later this month, we will be publishing the next steps regarding eligibility and pledging of LIBOR-indexed collateral including timelines around the requirements for fallback language and discontinuation of the LIBOR-index in pledged collateral.

As of December 31, 2020, approximately 13 percent of our membership is currently pledging LIBOR-indexed collateral. We don’t anticipate any changes to collateral currently pledged to FHLB Des Moines this year, but there will be eligibility changes for new pledges of LIBOR-indexed security and loan collateral moving forward.

Please refer to our

LIBOR Transition page on our website for all updates.

|

|

|

|

|

|

|

|

|

|

|

Members are Pledging eNotes!

|

This year, we've had several members complete implementation by transferring eNotes to our eVault and pledging eNotes to FHLB Des Moines! Ready to get started with eNotes? Visit the

eNotes resources on our website.

|

|

|

|

|

|

|

|

New Resource: Loan Collateral Eligibility - eNotes and Other Electronic Documents

|

|

|

Leaders from across the FHLBank System have collaboratively developed a new resource to answer questions that focus on the deployment of new technology and its impact on loan eligibility. This resource will be available on our website soon, but here's a preview of one of the Frequently Asked Questions:

What is preventing FHLB Des Moines from accepting eNotes in other eligible asset classes?

Answer: The infrastructure and market standards required to support eNotes in other asset classes is not yet established like it is for 1

-4 Family Residential First Mortgage Loans. There are many roadblocks to navigate including:

- The MERS® eRegistry is an integral part of our acceptance requirements as it allows FHLB Des Moines to control and perfect our security interest in 1-4 Family Residential First Mortgage Loans. At this point in time the MERS eRegistry does not accept eNotes for other asset classes and there is no other active industry registry that will accept eNotes for non 1-4 Family Loans.

- At this time, there is not an active secondary market for eNotes in other asset classes. FHLB Des Moines is required to ensure that the value for any collateral accepted to secure outstanding obligations can be readily and reliably determined. Given the lack of market data today, FHLB Des Moines cannot make this determination.

- The lack of defined and standardized documents prevents validation of the electronic record for other asset classes. The lack of standardized documentation creates interoperability issues between any potential Registry and an eVault to validate the eNote record.

|

|

|

|

|

|

Average Eligibility Factors Remain High Across Members

|

|

|

FHLB Des Moines establishes an Eligibility Factor (EF) after assessing eligibility and underwriting quality of a sample loan portfolio following your most recent Member Collateral Verification (MCV) review. The EF is one of the primary ratios used to calculate your institution’s

Advance Equivalent (AE), the maximum collateral amount available to members to secure extensions of credit.

|

|

|

Collateral Group

|

Average EF

|

Residential

|

91%

|

Commercial

|

90%

|

Agricultural

|

92%

|

|

|

|

Year after year, our members do an outstanding job at pledging only eligible loans. Looking back over the last four years, average eligibility from MCV reviews is around 90 percent (see graphic above). This high level isn’t surprising; FHLB Des Moines eligibility is rooted in large part by member and industry practices.

Looking to improve your Eligibility Factor? Read our article about

common causes of loan ineligibility. Verify you are pledging correctly, referencing our

Loan Eligibility Guidelines and Checklists. If you have more specific questions, a member of our

collateral team would be happy to chat with you either via email or phone.

|

|

|

|

|

|

What Collateral questions do you have?

|

|

|

|

|

|

|

Headline (H4)

|

|

We’re here to help support our members on all things collateral. From understanding an eligibility change to learning about new collateral types, we have many resources available. We want to hear from you! Is there anything you’d like to understand better within collateral? Submit your question by clicking the button below and we'll answer them in a future resource or Collateral Quarterly newsletter.

|

|

|

|

|

|

|

|

|

|

|

|

|

- The quarterly BBC reporting deadline was May 15, 2021. Members who have not yet updated their quarterly pledge have received a notification.

- We are in the process of adding an attestation to validate that your BBC pledge does not include 100 percent purchased participation loans.

|

|

|

|

|

|

|

Is there someone else on your team who should receive this newsletter?

|

|

|

|

|