|

REMINDER: LIBOR-Indexed Surveys are Due by March 9.

|

|

|

|

|

| |

|

COLLATERAL QUARTERLY

|

|

February 12, 2020 | Q1 2020

|

|

|

|

|

|

|

|

|

|

Future Acceptance of eNotes as Collateral within the Federal Home Loan Bank System

|

|

|

|

The 11 Federal Home Loan Banks (FHLBanks) are developing a solution that will pave the way for our members to pledge eNotes as eligible collateral. As member‐owned cooperatives, we recognize and understand the value and benefits that eNotes provide, both to our nearly 6,900 member institutions and to the customers they serve.

The FHLBanks have created Electronic Promissory Notes (eNotes) Collateral Acceptance Requirements and Guidelines—a common set of core requirements for accepting eNotes as collateral. These guidelines are based on federal law pertaining to electronic signature transactions, and set forth standards relating to eSignatures, eNote documentation, eClosings, eRegistry requirements, eNote vault requirements, and servicing system requirements.

The FHLBanks have made significant progress in arriving at a System-wide solution for storage of eNotes, and are in the process of finalizing this important milestone. Once this process is complete, the FHLBanks will be able to set a timetable for providing collateral value. However, since each individual FHLBank has its own systems, processes, and policies regarding collateral, implementation timelines will vary.

The Federal Home Loan Bank of Des Moines anticipates being operationally ready to accept eNotes in July 2020.

|

|

|

|

|

|

|

System Video: Accepting eNotes

|

|

|

|

|

|

LIBOR Survey: Responses are Due by March 9

|

|

|

Financial Markets to Phase Out of LIBOR by the End of 2021

At the end of September 2019, FHLB Des Moines received a letter from the deputy director of the division of federal home loan bank regulation. The supervisory letter stated the Bank must be able to identify and prudently manage the risks associated with termination of LIBOR in a safe and sound manner. Additionally, by December 31, 2019, the Bank must not enter into new financial assets, liabilities, and derivatives that reference LIBOR.

For members this means that before March 9, the Bank must determine the estimated loan collateral pledged that reference LIBOR—as well as to what extent pledged notes contain an alternative rate or other provisions, should LIBOR become unavailable or unreliable. FHLB Des Moines is collecting this information using a survey on the eAdvantage page.

Next Steps:

- Connect with your eAdvantage Team to ensure your institution has completed the first mandatory LIBOR-indexed Survey.

- If your institution has completed the first mandatory survey, there are no actions at this time. The next survey is not due until June 9.

- If your institution has not completed the survey, request this is completed on eAdvantage before March 9.

If your institution does not use LIBOR, the survey will only take about 10 seconds to complete. Questions may be directed to Advance Collateral at [email protected].

|

|

|

|

|

|

Lien Protection Products (LPPs) Eligibility Criteria Changes

|

|

|

|

The Bank is simplifying its criteria for acceptance of LPPs in lieu of traditional title work. LPPs are insurance products that reimburse lenders for losses realized from otherwise unknown superior liens. If an undiscovered superior lien on the property impairs the lender’s ability to collect or reduces the net proceeds upon its satisfaction, the LPP provider will pay the lender for losses incurred. Typically, lien position is assessed via a borrower affidavit of open liens and a check of the credit report for potential real estate mortgage loans.

|

|

|

|

|

|

|

|

|

|

Employee Feature: Cory Schoenherr

|

|

In late 2019, we welcomed a new addition to the Bank's Enterprise Risk division. Cory Schoenherr joined our Credit Risk Governance (CRG) team, assisting in Member Collateral Verification (MCV) support processes and reporting.

|

|

|

|

|

|

|

✔ REMINDER:

Quarterly Borrowing Base Certificate (BBC) Reporting Deadline is:

Friday, February 14

|

|

|

|

|

|

|

Spring is nearing and seasonal operating loans and lines are being renewed. During this time, we sometimes see loans that have past maturity. As a reminder, the Bank is unable to accept any loan and line that has past maturity without a renewal or extension having been executed by your institution and the borrower.

Consider the following to optimize loan collateral on this matter:

- For members listing loans and lines, advance equivalency is removed on any loans/lines past maturity. If you have large loans and lines renewing during this time, consider reporting more frequently during this period, notably after renewal of those loans or lines is complete.

- If you report collateral on a Borrowing Base Certificate, take a moment to review your supporting BBC loan detail to ensure removal of past maturity loans. In the event you have a Member Collateral Verification (MCV) scheduled, such loans could adversely impact MCV results.

Any questions should be sent to: [email protected].

|

|

|

|

|

|

Attention Loan Listing Members

|

|

|

Changes to the General File Format Start July 1

All members must add a "Rate Index" column to their file starting July 1, 2020.

Even if your institution does not pledge adjustable-rate loans, the column must be added.

This Rate Index column has been added at the end of the

General File Format to capture the index your institution is referencing regarding all adjustable-rate loans pledged to the Bank via a loan listing.

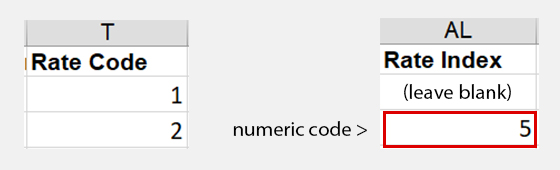

If the loan is a fixed rate loan and you have a 1 in column T, “Rate Code," leave the field in the new Rate Index column blank. If the loan is an adjustable rate loan and you have a 2 in column T, you will enter the numeric code that reflects the Rate Index (described below) in the new Rate Index column.

Continue using the current file through June 2020. If you use the new file before July 1, 2020, an error message will show upon upload to eAdvantage; Your file will not be processed until the column is removed.

On July 1, reporting the Rate Index on your file will replace the current LIBOR-Indexed survey prompt.

Numeric Codes for the Rate Index Column

1=Prime

2=SOFR – 1 mo

3=SOFR – 3 mos

4=LIBOR – 30 day

5=LIBOR – 60 day

6=LIBOR – 90 day

7=LIBOR – 6 mos

8=LIBOR – 9 mos

9=LIBOR – 12 mos |

10=Treasury – 3 mos

11=Treasury – 6 mos

12=Treasury – 1 yr

13=Treasury – 5 yr

14=Treasury – 7 yr

15=Treasury – 10 yr

16=Other |

|

|

|

|

|

The above image is a combined example; If 1 is listed under the Rate Code then the Rate Index is left blank. If 2 is listed under the Rate Code, 5 is entered under the

Rate Index to represent the LIBOR 60 day index.

|

|

|

|

|

|

Eligibility Notification: Term Out Lines of Credit

|

|

|

As outlined in the Bank’s Member Products Policy, all collateral:

- Must have a readily ascertainable market value;

- Can be reliably discounted to account for liquidation and other risks;

- Capable of being liquidated in due course; and

- The Bank must be able to perfect its security interest in the collateral.

Lines of credit agreements containing a borrower option to term out a portion(s) of the active credit line—without creation of a new closed-end promissory note and accompanying loan documentation—are not eligible collateral, as the Bank is unable to liquidate these loans in due course. This includes home equity lines of credit (HELOCs), commercial lines and agricultural lines.

The guidance herein does not impact the continued eligibility of lines of credit—which, upon end of the draw period, revert to a term out of the unpaid principal as governed by the credit agreement.

Questions may be directed to Advance Collateral at [email protected].

|

|

|

|

|

Is there someone else on your team who should receive this newsletter?

|

|

|

|

|